Hendersonville, Tennessee, strikes a perfect balance between peaceful lake living and the energy of nearby Nashville. With Old Hickory Lake as its backyard and downtown just a short drive away, it’s easy to see why so many buyers are setting their sights here.

But while the scenery is serene, the mortgage process in this competitive Middle Tennessee market can feel anything but. From understanding local prices to finding the right loan program, getting approved for a mortgage here takes a bit of insider know-how.

This mortgage Hendersonville guide walks you through everything you need to know to finance a home in this city—covering the latest market numbers, loan options, and financial assistance programs available to Tennessee buyers today.

Understanding the Hendersonville Market

Median Price Overview

In Hendersonville, the typical home value recently hovers around $513,734, with properties going pending in about 31 days. The median listing price was around $573,000 (up ~4.2% year-over-year) in August 2025.

Larger county-wide (Sumner County, TN) numbers show a median sale price of about $410,000 as of September 2025, with homes selling after roughly 69 days on market.

So what does that tell us? Hendersonville sits at the upper end of the local market—premium, but not out of reach (depending on your budget and timing).

Affordability Context

Compared with the broader Nashville metro, Hendersonville offers a combination of upscale amenities (lake access, good schools, community feel) and relative value—compared to some of the ultra-premium suburbs.

It’s “premium yet accessible.” But you’ll still need solid financing and a strong position to compete.

The Lender Advantage

Working with a mortgage lender Hendersonville who truly understands Sumner County can make a major difference in the homebuying process.

Local lenders are familiar with the area’s wide range of housing types—lakefront homes, established ranch-style properties, and newer subdivisions—and they understand the unique factors that can influence appraisals, such as flood zones or shoreline proximity.

They’re also more attuned to neighborhood-specific pricing trends and typical closing timelines. This local insight often translates to smoother transactions and stronger offers in a competitive Hendersonville market.

Choosing Your Loan Type

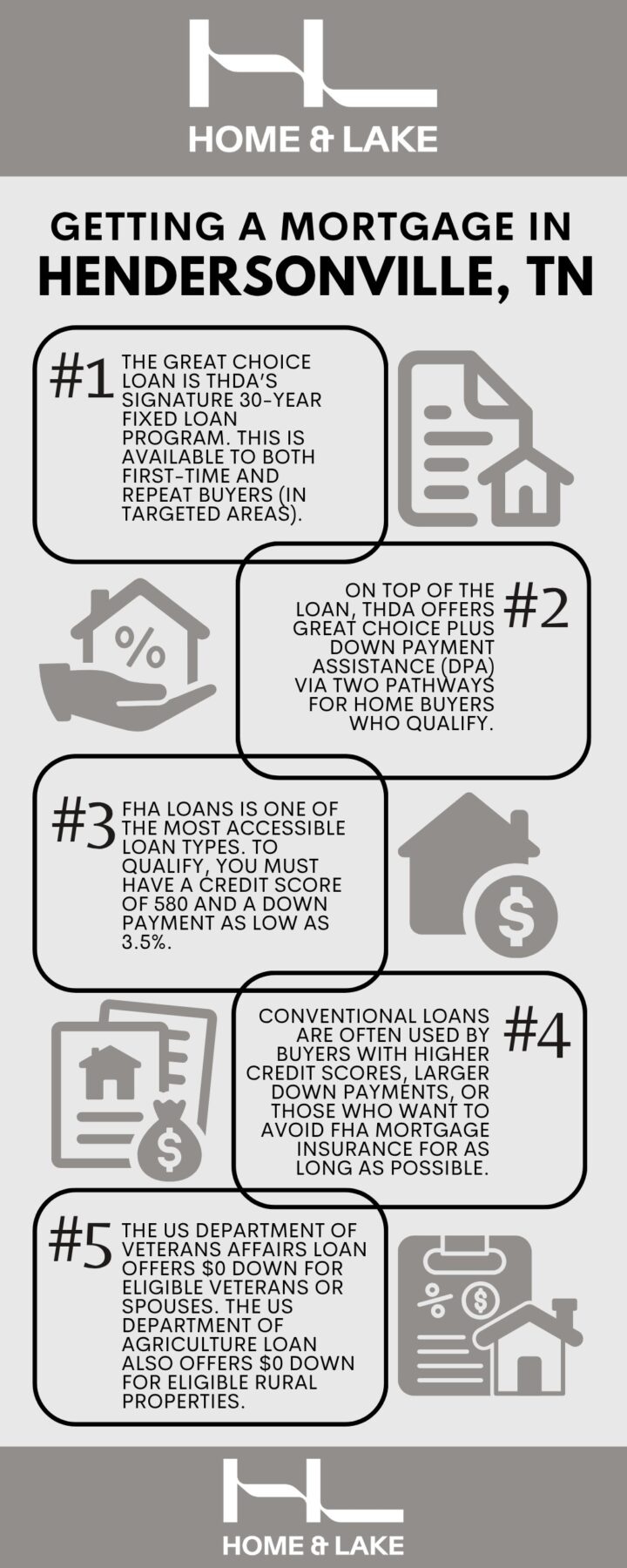

FHA Loans

One of the most accessible loan types—especially if your down payment is modest. With an FHA loan, you might qualify with a credit score of 580 (though some lenders prefer higher) and a down payment as low as 3.5%.

Also, for Tennessee, the one-unit FHA loan limit in higher-cost counties has been reported up to $989,000 for 2025. That means in many cases your Hendersonville purchase will be comfortably within FHA limits, which is great if you’re doing something above average but not “mega-mansion.”

Pro tip: Make sure the property itself meets FHA standards (condition, safety, structure) and don’t assume any old house qualifies without inspection.

Conventional Loans

Often used by buyers with higher credit scores, larger down payments, or who want to avoid FHA mortgage insurance for as long as possible. If you’re a first-time buyer, some conventional programs allow down payments as low as 3%.

For Tennessee/Metro Nashville-type markets, conforming loan limits for 2025 are reported at around $890,100 for one-unit homes in high-cost areas. So if you’re buying a single-family home in Hendersonville, you’re likely well under that ceiling—good news.

One reason to pick conventional: if you can manage more down payment and good credit, you may get more flexibility and lower insurance/fees.

VA and USDA

If you qualify, these are power moves. The U.S. Department of Veterans Affairs (VA) loan offers $0 down for eligible veterans or spouses.

The United States Department of Agriculture (USDA) loan for eligible rural properties also offers $0 down—but you’ll need to check eligible areas and income limits.

Even though Hendersonville is closer to suburban Nashville (not deep rural), some fringe properties may qualify. Always check location and program eligibility with your lender.

THDA: Your Key to Financial Assistance

This is one of the smartest moves a homebuyer in Tennessee can make. The Tennessee Housing Development Agency (THDA) runs programs designed for folks buying in places like Hendersonville or Sumner County—and they have real help to offer.

The Great Choice Loan

THDA’s signature 30-year fixed loan program. It’s available to both first-time and repeat buyers (in targeted areas).

- Eligibility: Minimum credit score of 640.

- Household income limits and purchase-price caps apply (varies by county).

- The rate is fixed, and you pair it with THDA-approved lenders.

Great Choice Plus Down Payment Assistance (DPA)

On top of the loan, THDA offers DPA via two pathways if you qualify:

- Deferred Option: Up to $6,000 given as a 0% interest second loan. No monthly payments—typically forgiven after 30 years if you live in the home and keep it as primary residence.

- Amortizing Option: Up to 5% of the sales price (max of $15,000) as a second Hendersonville mortgage with monthly payments. Same pairing principle.

These programs provide significant value by reducing the upfront cash required to purchase a home—an important advantage for buyers navigating Hendersonville’s competitive market and rising home prices.

Understanding the Full Cost: Closing & Taxes

Estimated Closing Costs

In Tennessee, expect closing costs to run around 1.18% of the sale price (as a ballpark) plus any lender/escrow fees, title insurance, appraisal, transfer taxes, etc. It’s smart to budget for more because each deal is different.

Major fees: appraisal, title insurance, escrow/settlement fee, recording/transfer taxes, lender origination, inspections.

Property Tax in Sumner County

Tennessee’s property tax system is less aggressive than many states.

In Sumner County, the county tax assessor evaluates property values and applies local millage rates.

While the rate will differ based on your location/municipality/school district, the cost tends to be relatively lower compared to many high-tax states. And that’s one reason this region is attractive.

Required Education

If you plan to use THDA’s DPA (Great Choice Plus), you’ll need to complete a THDA-approved homebuyer education course.

This can often be done online and is required before closing. Make sure you complete this early in your process so it doesn’t hold up your loan.

The Mortgage Checklist: Steps to Pre-Approval

Here’s your step-by-step prep list—consider this your go-to before house-hunting seriously.

Step 1: Credit Score Check

Check your FICO score (and your partner’s if applying together). If you’re going with a THDA program, the minimum is ~640. Conventional and FHA lenders may require higher down payments for the best rates.

If your score is under target, spend time boosting it (pay down debts, avoid new credit lines, etc.).

Step 2: Documentation Gathering

Start collecting:

- Last 2 years’ W-2s / tax returns

- Recent pay stubs (30–60 days)

- Bank statements (2–3 months)

- List of debts (credit cards, student loans, auto loans)

- Proof of down payment funds

Lenders will want to know you’re stable, reliable, and have the financials in order.

Step 3: Calculating DTI (Debt-to-Income)

Your DTI ratio = (monthly debt payments) ÷ (gross monthly income). Many lenders want this below 43% (some up to 50% depending on strengths). If your DTI is too high, your purchasing power shrinks. Use this as a guideline and clean up any unnecessary debts.

Step 4: Get a Local Pre-Approval

Using a local Hendersonville/Sumner County-familiar lender, get a pre-approval letter.

In this market, many offers will hinge on strong lender pre-approval, clear inspection/report timelines, and a lender who understands how to close quickly. A clean pre-approval helps you stand out.

Frequently Asked Questions

Is the THDA Great Choice Home Loan only available to first-time homebuyers?

No — while THDA initially focused on first-timers, the Great Choice Loan allows repeat buyers in many cases (especially in targeted areas).

What is the highest home price I can pay in Hendersonville and still qualify for a Conforming Loan?

Conforming loan limits for high-cost single-family homes in Tennessee are around $890,100 for one-unit homes per recent guidance. If your purchase is below that and you meet other criteria, you can use a conventional loan.

What credit score is generally required to access the best interest rates in the Hendersonville market?

For the best rates: typically 740 + (varies by lender). For many loan programs: FHA may allow ~580 for minimum down payment, but aiming for 620–640+ is safer. THDA requires 640+ for its loans.

Does the THDA $6,000 Deferred Option ever need to be repaid if I live in the home for the full 30 years?

If you live in the home as your primary residence for those 30 years and meet the program terms, the deferred second loan is forgiven—no monthly payment. If you sell or refinance early, you may owe pro-rata or all of it.

How does the property tax rate in Sumner County compare to Davidson County (Nashville)?

While specific millage rates differ by municipality, overall Tennessee property tax burdens tend to be lower than national averages, and Sumner County is generally competitive with nearby Davidson County. You’ll want to check the exact rate for your municipality, though.

Do I have to use a specific lender to access the THDA Great Choice programs?

Yes, you must use a THDA-approved lender to access the programs. The lender must be certified by THDA to originate those Great Choice loans and DPA options.

Can I combine the THDA Great Choice Plus assistance with a VA Loan?

No, THDA DPA is designed to pair with the THDA loan (Great Choice). VA loans have their own zero-down benefit but do not usually stack with THDA’s down-payment assistance programs. Always check with your lender for current stacking possibilities.

Key Takeaway

In Hendersonville’s competitive market, having a clean financial profile, the right lender, and strategic use of programs like THDA’s Great Choice Loan (and its down-payment assistance) can make all the difference.

You’re competing in a market where homes move—and move fast—so being prepared, clear, and locally aligned gives you the best shot at owning that lakeside-suburb retreat near Nashville.

If have any questions regarding this guide, or are interested to know more about the real estate offerings in Hendersonville, TN, feel free to give me a call today at 615-505-HOME or send me an email at britton@homeandlake.com to schedule an appointment.